|

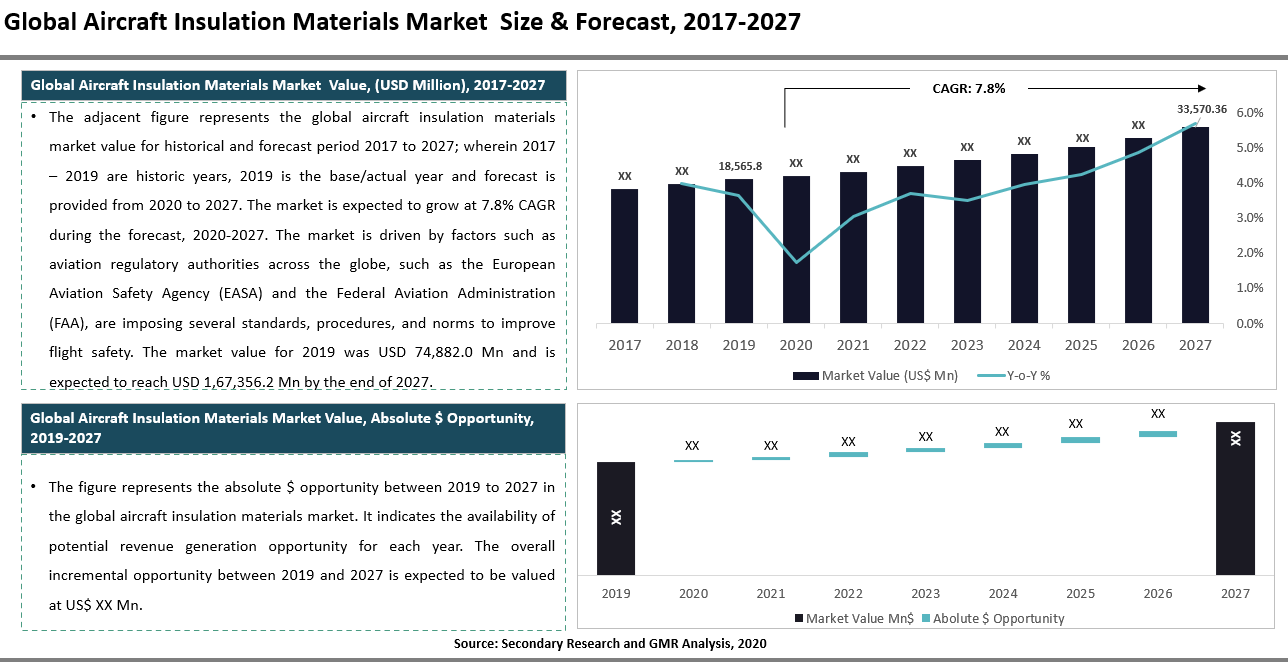

The global aircraft insulation materials market was valued at USD 18,565.8 Million in 2019 and is projected to reach USD 33,570.3 Million by 2027, expanding at a CAGR of 7.8% during the forecast period. The demand for lightweight aircraft in the military and commercial sector is growing, which, in turn, is boosting the usage of lightweight insulators. Many manufacturers in the aircraft insulation segment are investing heavily in research activities to develop and launch cost-effective and lightweight insulators, which can have modular functionalities and high recyclable components.

Thermal insulation market growth as FAA discarded the use of the insulation market in the year 2000 due to which thermal insulation was used as an insulation material. Thermal insulation is used all over the aircraft except few areas such as fuel usage below the passenger floor, crown area, and passenger cabins. In the aviation industry insulation material are used mainly for the safety of flight, reduction of noise & vibration and to provide comfort interior environment to passenger and crew. An increase in the insulation material is due to the rise in demand for safer aircraft operation and lightweight aircraft in both civil and military aviation. In this segment, the civil aviation market is excepted to lead the market as there is an increase in the production of civil aircraft due to the rise in air travelers and also government all over the world are spending more funds to build better aviation infrastructure so that they could connect all the cities.

Thermal insulation market growth as FAA discarded the use of the insulation market in the year 2000 due to which thermal insulation was used as an insulation material. Thermal insulation is used all over the aircraft except few areas such as fuel usage below the passenger floor, crown area, and passenger cabins. Acoustics insulation materials provide a high-efficiency and minimum amount of volume and weight due to which it is extensively used in aircraft. Electric insulation provides protection from sensitive electric systems and other components of aircraft from heat and interference. Thus, it is mostly used in backplates, switchgear, switchboards, flexible laminates, and winding wires.

Market Dynamics

The market is driven by factors such as demand for lightweight aircraft in the military and commercial sector, imposing several standards, procedures, and norms to improve flight safety boost the usage of aircraft insulation materials across the world.

Increasing Demand for Cost-Effective and Lightweight Insulators

Many manufacturers in the aircraft insulation segment are investing heavily in research activities to develop and launch cost-effective and lightweight insulators, which can have modular functionalities and high recyclable components.

Strengthen Regulation to Ensure Usage of Safety Materials

Aviation regulatory authorities across the globe, such as the European Aviation Safety Agency (EASA) and the Federal Aviation Administration (FAA), are imposing several standards, procedures, and norms to improve flight safety.

High Labor Cost and Strict Rules in Associated Industry

High labor costs and lack of efficient recycling technology for insulation materials are expected to restraint the growth of the aircraft insulation market. Moreover, EASA, FAA, and other aviation organizations are imposing strict rules on paint manufacturing and chemical companies, which is leading to products having a limited shelf life, thus needing replacement at regular intervals. These factors are estimated to restrain the growth of the market due to their less stability.

Opportunity in Composite Material Category

Increasing demand for the usage of composite materials is expected to create opportunities for the aircraft insulation market players. These materials can help reduce noise and vibration while increasing fire safety. An increase in the number of electric components in aircraft is projected to fuel the growth of the market.

Growing Travel Trend and Rise in Investment to Boost the Industry Further

An increase in the production of aircraft, a surge in air travel, a rise in living standards in developing countries, and growth in the number of low-cost airlines have increased the production of insulation materials.

The rise in investments to make aircraft lightweight for the military and commercial sectors are increasing the demand for aircraft insulation materials.

Segmental Outlook

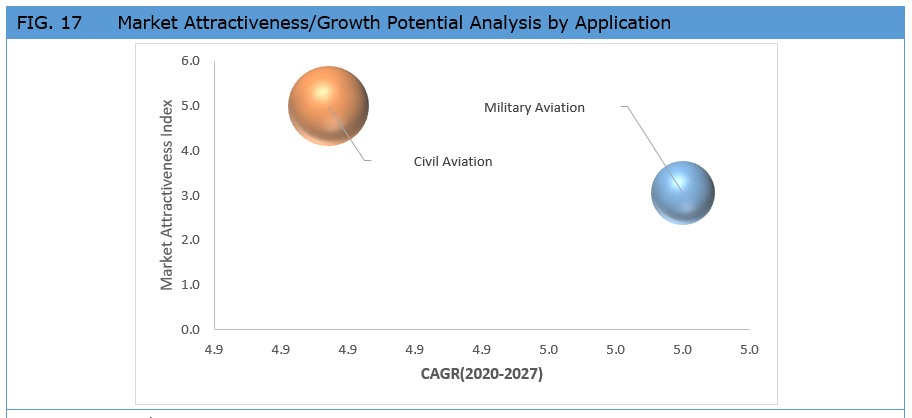

On the basis of types, the aircraft insulation materials market has been segmented into thermal, acoustic & vibration, and electric insulation. Thermal insulation plays a vital role in maintaining a comfortable environment while the aircraft is in the air owing to these thermal insulation materials being used significantly in the aircraft. Material segment is expected to grow highest at 9.1% during the forecast as compared to insulation type. Foamed Plastics category holds the highest value share in the materials segment. Based on application, the market is fragmented into military aviation, civil aviation. Civil aviation holds the highest value share 62.0% in 2019 however, military aviation is expected to expand highest 6.3% during the forecast, 2020-2027.

Based on sales channels, the Aircraft insulation materials market has been segmented into manufacturers, distributors, and service providers. The manufacturer’s category holds the highest value share (62.5%) in the global market in 2019 and also is expected to expand at the highest CAGR, 7.9% during the forecast. The distributor segment is also expected to grow at a significant pace during the period. Aircraft insulation manufacturers are projected to hold the largest share over the assessment period. Boeing is one of the major aircraft manufacturers worldwide. Boeing is insulating its latest airplanes models with Basotect, BASF’s heat & sound insulating melamine resin foam. This is the first time that a BASF foam is applied in the mass production of acoustic insulation for airplane cabin walls. Aircraft insulation manufacturers highly depend on Aircraft insulation materials distributors to manufacture the custom aircraft parts as per the requirement. This, in turn, increases the demand for insulation materials distributors.

Regional Outlook

In terms of regions, the market has been segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. North America is a promising region for the market. It constituted a 45.7% share of the market in 2019. The North America market in the region is projected to expand at a CAGR of 8.1% during the forecast period. Huge spending on defense aircraft and the military is driving the regional market growth. Also, the presence of major industry players such as Triumph Group Inc., Esterline Technologies Corporation, and DuPont, is further propelling the market rise. The Asia Pacific is estimated to witness high growth during the forecasted time. A lot of numbers of aircraft have to be delivered by Boeing in upcoming years in the Asia Pacific region. Mainly the demand is been originated from China, India, and Japan. Other supporting drivers in the region are the opening of assembly plants of Boeing in this region. Moreover, there is growth in investments in new airport development in the Asia Pacific, due to which there are opportunities for aircraft insulation materials adoption.

|