Market Outlook:

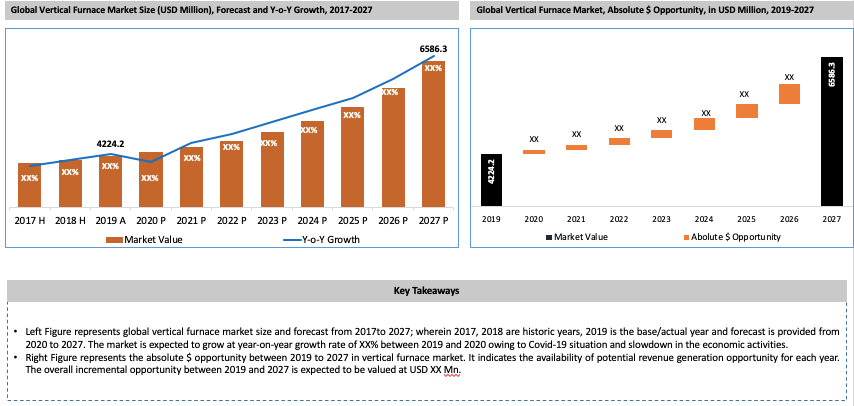

The global vertical furnace market was valued at USD 4,224.2 Million in 2019 and is projected to reach USD 6,586.3 Million by 2027, expanding at a CAGR of 5.4% during the forecast period. Booming consumer products and electronics sector in several developed economies such as China and Japan have resulted in the expansion of the semiconductor industry, which is in turn, boosting the growth of the vertical furnace market. Furthermore, developments in technology for improving the thickness uniformity are creating opportunities in the global vertical furnace market. Vertical furnaces provide a much higher performance, as compared to horizontal furnaces, in terms of temperature uniformity and cleanroom footprint. Moreover, they provide improved wafer handling by moving carrier up rather than using long (transversally loaded) cantilevers, making it suitable for advanced manufacturing of semiconductors and advanced packaging.

Market Dynamics

The demand for vertical furnaces is rising as they are used for advanced packaging, which are used for improving the device performance, high demand for semiconductor products, and growth in application of vertical furnaces are the major factors boosting the market. Conversely, high cost of products, and unaffordable price for small enterprise in the semiconductor are expected to restrain the growth of market. Rise in R&D investments and developments in wafer size at decreasing costs are anticipated to create lucrative opportunities in the market.

Segmental Outlook

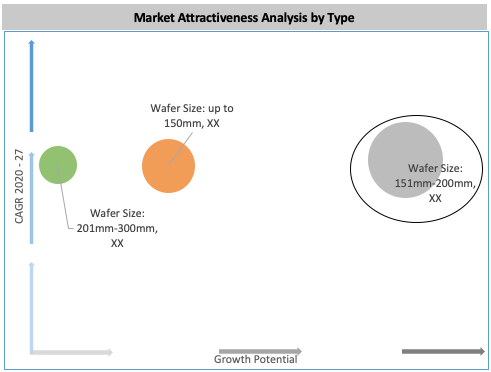

Based on types, the market has been segmented into wafer sizes: up to 150mm, wafer size: 151mm – 200mm, and wafer size: 201mm – 300mm. The wafer size: 201mm – 300mm segment dominated the overall market in 2019 with share of 69.4%. The large share of the segment is attributed to the high demand for several IC products, which are made from semiconductors such as flash memories, power management devices, and image sensors, which are built on furnaces with 300mm wafers.

On the basis of methods, the market is segregated into LPCVD, PECVD, thermal oxidation, and others. The LPCVD segment is estimated to expand at a CAGR of 5.8% during the forecast period. The growth of the segment is attributed to its high usage due to its various attributes such as high purity, thickness uniformity, and superior reliability.

By Type

Trends

The wafer size: 201mm – 300mm segment holds a significant share in the market and is projected to grow at a substantial pace during the forecast period owing to its ability to aid a large number of device manufacture in a single batch. This also helps reduce the overall cost/unit as compared to other wafer sizes. Moreover, high demand for IC products such as CPUs, GPUs, DRAM, NAND flash, power management devices, image sensors, and other high-volume technologies are typically built on 300mm wafers, which ultimately results in the growth of the segment. Regardless of its diminishing demand and short-term outlook, it is expected that vertical furnace 151mm – 200mm wafers will still remain viable during the forecast period as all wafer-based products do not require advanced nodes, which are provided by wafer size: 201mm – 300mm. However, depletion in the supply of and use of refurbished wafer size: 151mm – 200mm is anticipated to limit the growth of the segment. OEMs are manufacturing new 200mm equipment, which integrate 300mm technology to mitigate supply constraints.

By Application

Definitions

Advanced Packaging: Advanced packaging is a common classification of a number of distinct technologies including 2.5D, 3D-IC, wafer-level fan-out packaging, and system-in packaging. Advanced packages such as fan-out and those introduced through silicon vias (TSVs) have become core packaging platforms that effectively address the latest trends. These types of advanced packaging techniques provide the requisite modularization and convergence to allow higher output levels at the system level, offering greater bandwidth, and provide efficient power management. In advanced packaging, vertical furnaces are used for providing high yield anneals for e-WLB and thermal processes for interposer TSV. Moreover, it provides wet thermal oxide for Si through liner with high conformity and oxide integrity, controlled film shrinkage, and bowing. Vertical furnaces help with low-temperature metal anneals with strong sheet resistance (Rs), low CoO, and low O2 atmosphere, which prevents Al or Cu oxidation.

Semiconductors: Semiconductors are materials that provide conductivity between conductors (usually metals) and non-conductors or insulators (such as most ceramics). Semiconductors can be pure elements, such as silicon or germanium, or derivatives such as gallium arsenide or cadmium selenide. Small amounts of impurities are applied to pure semiconductors in a doping process, which causes drastic changes in material conductivity. Vertical furnaces for annealing and thin film formation are broadly used in the manufacturing semiconductor devices, as it provides exemplary temperature distribution, and atmosphere control.

Regional Outlook

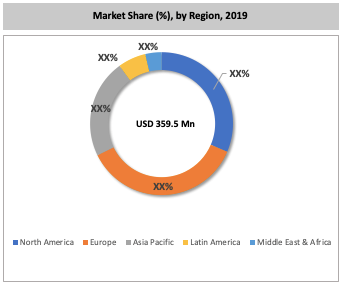

On the basis of regions, the market is classified as North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. The demand for vertical furnaces in North America is projected to expand at a CAGR of 5.3% during the forecast period owing to the large investments in high-end products such as wearables, IoT devices, and advanced computing devices. These premium products require advanced packaging on semiconductor which increases the cost of the final products. the demand for these premium products is increasing in the region, which in turn is expanding the demand for vertical furnaces in the region.

The demand for the vertical furnace in Europe is projected to expand at a substantial CAGR during the forecast period. The market in this region is driven by the presence of several automotive manufacturers that use automotive semiconductors such as sensors, processors, and power devices. These semiconductors are also used for the production of vehicles; therefore, the rise in the demand for automotive semiconductors is expected to boost the vertical furnace market in the region.

Competitive Landscape

- Key players in the global vertical furnace market includes ASM International, Centrotherm international AG, Koyo Thermo Systems Co., Ltd., Tempress, Tokyo Electron Limited, and Kokusai Electric Corporation. These companies are considered as key manufacturers of vertical furnace, based on their revenue, research & development activities, regional presence, and supply chain management system.

- The players are adopting key strategies such as acquisition, and geographical expansion where potential opportunity for the Vertical Furnace extraction is added in the company’s capacity.

- In July 2019, Kokusai Electric Corporation expand its collaboration with Grenoble’s Substrate Innovation Center (France) associated with Soitec (Euronext Paris), a leading designer and manufacturer of innovative semiconductor materials for R&D activities.

- In April 2019, Centrotherm International AG introduced new system generation for PECVD and LPCVD processes and solar cell concepts with passivated contacts which is intended to enable solar cell manufacturers to achieve further significant increases in efficiency.

- On January 2019, Koyo Thermo Systems Co., Ltd updated the VF-3000 Low Cost Mini Batch Vertical Furnace with features such as a low temperature LGO heater, optimized the heat efficiency, and heat dissipation balance of the operating temperature range insulation, and manufactured and conducted a heater prototype.

- In July 2017, ASM International launched Intrepid ES(TM) 300mm epitaxy (epi) tool for advanced-node CMOS logic and memory high-volume production applications.

|